Around 9 million Australians own Total and Permanent Disability (TPD) insurance, with most obtaining it through their superannuation fund. TPD insurance generally pays a lump sum benefit if you’re injured or critically ill and unlikely to ever work again. But understanding how TPD payouts work—especially when they come through your super—can be confusing.

This guide covers everything you need to know about TPD payouts: how they work with super funds, tax implications, and practical strategies to maximise your benefit.

Key Takeaways

Figuring out TPD payouts can be confusing, so here’s what actually matters:

- Your super probably already covers you for TPD—usually $60k to $500k, depending on your age

- TPD payouts from insurers are tax-free, but if it comes through your super, you might pay up to 22% tax depending on your age

- When your claim’s approved, the payout lands in your super and you can access all your super early too

- Your tax bill depends on how old you are, whether you take a lump sum or income stream, and how much of your super is already tax-free

- You can take it as regular income, withdraw it in one go, or just leave it there for now

- You can lower your tax by using the tax-free uplift, timing your withdrawal right, or choosing an income stream over a lump sum

- Tax depends on your age—keep it in super and there’s no immediate tax hit

- Most people get the calculations wrong—especially around tax-free amounts and work dates—so it’s worth chatting with a financial adviser

Can I Get a TPD Payout From a Superannuation Fund?

Yes, absolutely. A number of super funds provide TPD insurance automatically as part of a group insurance policy that covers numerous members simultaneously. Under these policies, the super fund offers a pre-determined amount of TPD cover, typically based on your age. Superannuation is the most common ownership structure for TPD insurance in Australia, and you can receive a TPD payout from a superannuation fund.

You can often exercise some control over how much TPD cover you receive through your super. Many people contact their super fund directly to apply for coverage up to a preferred amount. However, note that this coverage may decrease as you get older. It may also increase with changes to the consumer price index (CPI). Additionally, when increasing your cover, your super fund is likely to ask you questions relating to your health which may prevent you from obtaining the cover you desire.

Depending on your super fund, you may be able to fix the amount of cover you have. This tends to come at the cost of higher monthly premiums, especially as you get older. Requests to change the TPD insurance you receive via your super may also lead to the super fund asking questions about your medical health, current working status, and age before accepting your request.

What Is the Minimum Payout for a TPD Claim?

The minimum TPD payout from a superannuation fund varies depending on the nature of your policy. Payouts tend to range between $60,000 and $500,000, with an approximate average of $250,000 for insurance that is provided directly by a super fund. Where your cover has been established by a financial adviser, you are often able to insure for in excess of $3,000,000.

You can see the figure that applies to you on your superannuation membership statement or your latest renewal notice. You may be able to speak to your super fund to increase the size of your payout if you’re willing to pay higher premiums.

How Does a TPD Insurance Claim Work With Super?

Initially, making a TPD claim through your super fund works the same as claiming with an individual policy. You contact your insurer or super fund to inform them of your condition. The insurer collects evidence demonstrating you have an injury or disability that prevents you from working. It then decides whether to grant the claim based on the evidence collected.

That said, the claims process for all TPD policies is quite complex with many different sets of criteria that need to be satisfied for your claim to be accepted. Engaging a TPD Claims Adviser can help you in mitigating the risk of unforeseen issues as well as ensuring the process is handled efficiently.

Assuming your insurer accepts your claim, the policy’s benefit is paid into your superannuation account. In addition to being directly added to your super’s balance, this payment triggers your ability to access the funds in your super. That’s due to TPD benefits only paying out if you can no longer work. Think of it as your super classing you as retiring, thus granting you access to your funds.

Is a TPD Payout Taxable?

This is where things get a bit more complex. The answer depends on how you hold your TPD insurance.

A TPD insurance lump sum payout made outside of superannuation is typically tax-free and is not considered income. However, where a TPD payout is made through super, there are several factors you need to consider as your benefits may be taxed.

The key questions are:

- Is your payout lump sum or an income stream?

- Is it paid to super or directly to you?

- How old are you?

Lump Sum Payout

When accessing a TPD lump sum payout that has been received through super, there may be an element of taxation. Essentially, superannuation balances are comprised of tax-free and taxable components which materially impact the net benefit you will receive upon withdrawal. Your Super Fund should be able to provide you with precise figures relating to the breakdown of your fund, enabling you to better understand your tax liabilities. You may read more about the details from the Australian Tax Office website here.

Where your policy is held in your own name and paid directly to you, it is unlikely that you have a tax liability however you should consult a tax advisor to confirm this.

Income Stream Payout

TPD payouts that are paid as an income stream can be deemed as taxable income. You may be eligible to receive an offset on the taxable component of the income stream which reduces your tax liability however you will need to consult a licensed tax advisor to confirm how this will apply to you.

What Tax Will You Pay on a TPD Payout?

The rate of tax typically applied to the taxable component of your TPD payout will be 22%. This assumes that you are under preservation age which is common among those receiving such payouts. The amount of tax you will pay is entirely dependant on your own circumstances which makes it crucial that you seek advice when determining this amount.

What Is the Percentage of TPD Taxed on Your Payout?

Knowing how much you owe in taxes for your TPD payouts is important as it will affect how much you can take home and spend for your needs.

Here’s a quick guide you can use to give you an idea of how much tax you should pay for TPD payouts within your super:

If you are above the preservation age (55-60):

- Lump sum withdrawals shall be tax-free

- Withdrawing as an income stream could also be tax-free depending on the taxable portion of your superannuation balance

If you are below the preservation age:

- Lump sum withdrawals can be taxed of up to 22%

- Income stream withdrawals will be taxed at each individual’s marginal tax rate less 15% tax offset

Calculating the tax on TPD payout can be a bit overwhelming. If you need an expert to work with you on this, talk with our TPD Insurance Claims Advisers today.

The Superannuation Preservation Age

Knowing the preservation age is important as it will greatly affect your tax dues once you reach your preservation age.

| Date of Birth | Preservation Age |

|---|---|

| Before 1 July 1960 | 55 |

| 1 July 1960 – 30 June 1961 | 56 |

| 1 July 1961 – 30 June 1962 | 57 |

| 1 July 1962 – 30 June 1963 | 58 |

| 1 July 1963 – 30 June 1964 | 59 |

| From 1 July 1964 | 60 |

What Happens After I Receive My TPD Payout?

Once you gain access to your super funds, you have three options:

- Create an income stream using the balance in your super

- Withdraw the total or a partial amount of your benefit

- Leave the funds in your super, so they can continue to mature

Some supers also allow you to make a partial lump sum withdrawal before you use the rest of the benefit to contribute to an income stream.

Depending on your age and when you created the super, you may have to pay tax on withdrawals. If you’re currently under the super’s preservation age, you’ll pay tax on any income stream you create at a marginal rate, minus a 15% tax offset. Withdrawing the TPD benefit means you pay a lump sum tax, which varies depending on your age and the amount you withdraw. You don’t pay any tax on the benefit if you leave it in your super, though you may have to deal with taxes if you withdraw money in the future.

Once you receive your TPD payout, you have a few options on what to do with your benefit. Understanding these options fully can help you make the best decision for your circumstances.

How to Reduce Your TPD Tax

Lower tax being imposed on a TPD payout means more funding for your needs. Below are four ways on how a person can minimise their tax obligations when receiving a TPD payout legally:

- Understanding the Tax-Free Uplift – if you withdraw your payout through your super account, there’s a tax-free uplift calculation that may substantially lower your taxed amount.

- Know the right time to withdraw – You may not be compelled to withdraw your payout immediately and you may have numerous options available to you. Understanding these options, in full, can result in better outcomes for your circumstances.

- Consider the Income Stream option – for people who are under the preservation age, having your TPD payout in an income stream option may lower your tax rather than having it in a lump sum.

- Get help from a professional – navigating your TPD insurance payout, superannuation and taxes could get you lost and confused. An expert adviser can guide you through the process, providing you with security and comfort.

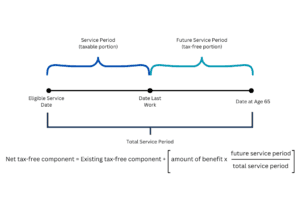

Guide to How TPD Tax Is Calculated

Learn how your TPD tax is calculated in relation to the tax-free uplift. Below is a guide illustration that you can follow.

What to Know About Calculating TPD Tax

When making a TPD payout withdrawal on your super account if you’re below the preservation age, you need to have these information available:

- Your date of birth – in order to get your preservation age

- Eligible Service Date – this is when your superannuation account was created. In case you managed to combine multiple superannuation accounts, you need to consider the earlier eligible service date

- Date Last Worked – this pertains to the date of your termination from your employer, not the date of having been diagnosed with your medical condition or disability

Common Problems With TPD Tax Calculations

When dealing with TPD tax calculations, it is very common that one might get it wrong if one tries to calculate it themselves. Here’s a list of common problems others have faced:

- Misinterpretation of the Tax-free component – most people are incorrectly computing the tax-free portion of their TPD payout

- Incorrect Tax Withholding – there are cases of super funds withholding incorrect amounts of taxes resulting in over or underpayment

- Obsolete information on Tax Laws and Regulations – when navigating your way in taxes, one must make sure that the knowledge and information about the matter is up to date as the rules and regulations in taxes are subject to change

- Not aware of Income Stream Option – receiving the TPD payout as an income stream can be advantageous for tax purposes

- Do-It-Yourself Approach – getting your taxes right saves you money but will cost you greatly should you fail. Getting help from financial professionals will not only save you money but time as well.

What If There Was a TPD Calculation Error?

In the event of being overtaxed, your TPD tax calculation is probably where the problem started. Either you or your super fund might have used the wrong date for your last work. Double-check your calculation or have a financial expert look at it for you.

Our TPD Tax Calculator Tool might give you an idea of your tax dues.

The Right Super for Potential TPD Claims

Appropriate research helps determine if you have the right super for potential TPD claims. The following steps allow you to learn more about your super and make adjustments based on your needs:

- Check your existing super account to see what, if any, automatic TPD coverage you already have. Once you know how much you can claim, contact the super fund if you wish to increase or change your TPD cover.

- When adjusting your benefit, think about the impact that being unable to work would have on you and your family. As you’ll lose your primary source of income, you need to ensure the benefit is high enough to maintain your standard of living if you stop working. Furthermore, it would help if you accounted for any additional costs related to care.

- Compare your super’s TPD coverage with standalone policies. You may find that an individual policy offers superior coverage at a lower premium. Having a personal policy also gives you more direct access to your benefit without the tax implications that result from withdrawing that benefit from a super.

- Speak to an independent financial advisor if you’re unsure about your TPD insurance needs or the implications of linking your TPD cover to your super.

- Read all exclusions, definitions, and release conditions in the linked TPD policy to ensure you don’t get caught out by any surprises if you need to claim. Contact your insurer or super provider if you’re unsure about any of the terms you see in the paperwork.

Do TPD Payouts Impact Centrelink Payments?

TPD payouts can affect your Centrelink payments as it may reduce the amount once you withdraw from your superannuation funds. Centrelink takes into consideration the individual’s current financial status if you’re eligible and the amount of payment. You may read our separate guide on what to do after your TPD payout gets approved.

Frequently Asked Questions About TPD Payouts

What is the average TPD payout?

TPD payment amounts vary drastically in Australia. The amount can range from $50,000 to in excess of $5,000,000 depending on your policy. The average Total Permanent Disability payout from a superannuation fund in Australia is around $250,000. A standalone policy may provide a different average payout amount as you generally have the ability to insure for a greater amount when coverage is established through a financial adviser.

Is a TPD payout taxable?

This depends on whether you obtain your TPD insurance from an independent insurer. This is usually tax-free as its payout is not considered as income. However, should the payout be from your super account, several factors can make a portion of your withdrawal taxable between 18% – 22%.

How much tax will I pay on my TPD payout?

The standard marginal income tax rate is 22%. However, with the tax-free uplift calculation, your tax due can decrease between 18% – 1%.

How much is a lump sum payout for TPD?

There are several factors that can determine your TPD payout such as insurance coverage, income, and level of disability. Payouts typically range from $60,000 to $500,000 through super funds, with an average of $250,000.

What happens after a TPD payout?

Upon receiving your TPD payout, you have the following options:

- Withdraw a lump sum amount or partial withdrawal

- Use your super balance to have an income stream option

- Leave the funds in your super to continue maturing

Are TPD payouts considered taxable income?

Should you withdraw your TPD payout as a lump sum it is unlikely to be treated as taxable income however it is likely that tax will be payable on the lump sum prior to you withdrawing the funds. There are many variables when determining how much tax will be taken from your payout and this information can generally be provided to you by your super fund prior to finalising the claim.

Can you return to work after receiving a TPD payout?

The short answer is yes. There is no time limit placed on an individual returning to work after they have received a total and permanent disability payment however it is unlikely you will be able to establish a new TPD policy after you have had a TPD claim approved.

How Curo Can Help Maximise Your TPD Payout

Our team has decades of knowledge and expertise in the industry which allowed us to navigate the complexities of TPD payouts, superannuation, and taxes. This is our way of looking out for our clients and because this is what matters in what we do.

We’re specialists in complex TPD claims, including those involving superannuation funds. No matter who provides your cover, we can help you:

- Make claims efficiently and professionally

- Understand and minimise your tax obligations

- Navigate the complexities of TPD payouts through super

- Maximise your benefit while reducing your tax burden

Talk to our team of TPD Insurance Claims Advisers today and we will work with you so that you can get the most out of your insurance when you need it the most.

General Advice Disclaimer

General advice warning: The advice provided is general advice only and in preparing it we did not take into account your investment objectives, financial situation or particular needs. Before making an investment decision on the basis of this advice, you should consider how appropriate the advice is to your particular investment needs, and objectives. You should also consider the relevant Product Disclosure Statement before making any decision relating to a financial product.

Check Your Eligibility for a TPD Claim

Take a short assessment to see if you may qualify for a Total and Permanent Disability claim. It’s quick, private, and helps you decide your next step.

- 2–3 minutes

- No obligation

- Confidential

You'll get guidance based on your answers.

Last Updated on April 17, 2026 by Brent Satill